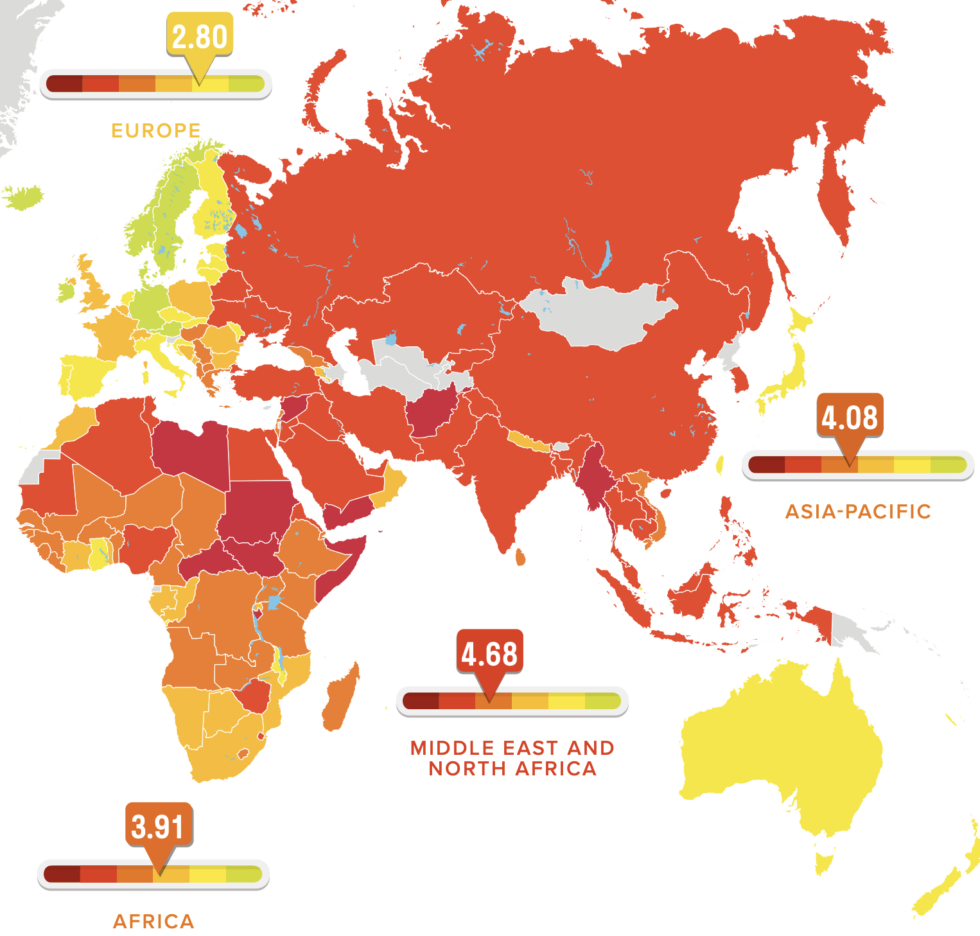

The World’s Worst Countries for Workers

The only comprehensive, global annual survey of the violation of workers’ rights

Among the most shocking data points in 2026 are a five percentage point rise in violations of free speech and assembly over the past year, a six percentage point increase in violent attacks against workers, and a three percentage point rise in attacks on civil liberties, including a dramatic rise in the number of arrests and detentions of workers and their representatives. The sharp spike in these indicators signals that the persecution of trade union leaders is becoming commonplace in an ever-growing number of countries.

Increasingly, we see new technology being deployed as a method of control, used to monitor, discipline and silence workers. We also see fewer governments consulting unions in good faith before amending or introducing labour laws.

In Europe and the Americas, workers’ rights are suffering an alarming decline. Both regions registered their worst average country rating since the Index began in 2014 and the increasing influence of the far right is putting workers and unions at risk in countries such as Argentina and France – two out of four countries to be downgraded in 2026.

[ > International Trade Union Confederation — 2026 ]

28 definition

28 ʞuɐ⊥-ʞuᴉɥ⊥ DEFINITIONS :

– Addiction to Peace – Re-Civilization – Post-Aid World – ‘Liberal’ Fatwa Machine – Burden-Dropping – Peace Renewable Energy Credit – Whataboutism – Bow Wave – Japanification – WhatsApp World Order – Stellar City – Agentic State – Security Poverty Line – Ontological Security , Anthropocentrism – Biosecurity – CRANKs – Pax Trumpica – Axis of Upheaval – Trumponomics – Zero Emission Neighbourhoods – Secretonomics – Paratransit – Environmental Racism – Fossil Fashion –

Diplomatie de l’indifférence – Rayonnement territorial des entreprises –

June 2026

China Green Finance Status and Trends 2025-2026

China’s green finance development in 2025 continued to make significant progress across several areas. This advancement contrasts with trends in many Western markets, which have slowed or, in the case of the United States, reversed progress on green and sustainable finance.

[ > Green Finance & Development Center — February 24, 2026 ]

54 top Chinese think-tanks

Demography :

UNFPA in China

-, china.unfpa.org en + zh

Economic think-tanks :

中国经济50人论坛

[ China Economic 50 Forum ]

Beijing, 50forum.org.cn zh

Asian Infrastructure Investment Bank

Beijing, aiib.org en

American Chamber of Commerce in the People’s Republic of China

Beijing, amchamchina.org en

Hong Kong Academy of Finance

Hong Kong, aof.org.hk en

Central Asia Regional Economic Cooperation Institute

Urumqi, carecinstitute.org en

China Center for International Economic Exchanges

Beijing, cciee.org.cn en + zh

China Development Institute

Shenzhen, cdi.org.cn en + zh

Institute of World Economics and Politics

Beijing, iwep.org.cn en + zh

European Union Chamber of Commerce in China

Beijing, europeanchamber.com.cn en

EU SME Centre

Beijing, eusmecentre.org.cn en

Hinrich Foundation

Hong Kong, hinrichfoundation.com en

Hong Kong Monetary Authority

Hong Kong, hkma.gov.hk en + zh

中国社会科学院金融研究所

[ Institute of Finance, Chinese Academy of Social Sciences ]

Beijing, ifb.cass.cn zh

National Institution for Finance & Development

Beijing, nifd.cn en + zh

北京大学新结构经济学研究院

[ Peking University Institute of New Structural Economics ]

Beijing, nse.pku.edu.cn zh

Chongyang Institute for Financial Studies (Renmin University of China)

Beijing, rdcy.ruc.edu.cn en + zh

北京大学 国家发展研究院

[ National School of Development, Peking University ]

Beijing, nsd.pku.edu.cn zh

Economic & social think-tanks :

南都公益基金会

[ Narada Foundation ]

Beijing, naradafoundation.org zh

Energy :

中国石油集团经济技术研究院

[ China National Petroleum Corporation Economics and Technology Research Institute ]

Beijing, etri.cnpc.com.cn zh

Green think-tanks :

Civic Exchange

Hong Kong, civic-exchange.org en + zh

Energy Foundation China

Beijing, efchina.org en + zh

全球环境研究所

[ Global Environmental Institute ]

Beijing, geichina.org zh

Green Finance & Development Center (Fudan University)

Shanghai, https://greenfdc.org/publications/ en

Human rights :

China Human Rights

Beijing, https://en.humanrights.cn/2025/index.html en + zh

International Relations :

Asia Global Institute (University of Hong Kong)

Hong Kong, asiaglobalinstitute.hku.hk en

Boao Forum for Asia

Beijing, boaoforum.org en + zh

Carnegie China

Beijing, carnegieendowment.org/china en

Centre on Contemporary China and the World

Hong Kong, cccw.hku.hk en

Center for China & Globalization

Beijing, ccg.org.cn en + zh

China-US Focus

Hong Kong, chinausfocus.com en + zh

China Institutes of Contemporary International Relations

Beijing, cicir.ac.cn en + zh

China Institute of International Studies

Beijing, ciis.org.cn en + zh

China-United States Exchange Foundation

Hong Kong, cusef.org.hk en + zh

Development Reimagined

Beijing, developmentreimagined.com en

Institute of International and Strategic Studies Peking University

Beijing, iiss.pku.edu.cn en + zh

Shanghai Institutes for International Studies

Shanghai, siis.org.cn en + zh

Greater Tumen Initiative

Beijing, tumenprogram.org en

International security :

Center for International Security and Strategy (Tsinghua University)

Beijing, tsinghua.edu.cn en

Grandview Institution

Beijing, grandview.cn en + zh

Institute of European studies (CASS)

Beijing, ies.cass.cn en + zh

Multidisciplinary :

Friedrich-Ebert-Stiftung China

Beijing, china.fes.de en + zh

中国改革网

[ China Reform Network ]

Beijing, chinareform.net zh

中国改革发展研究院

[ China Institute for Reform and Development ]

Haikou City, Hainan Province, chinareform.org.cn zh

中国智库网 (国务院发展研究中心)

[ China Think Tank Network (Development Research Center of the State Council) ]

Beijing, chinathinktanks.org.cn zh

Heinrich-Böll-Stiftung / Beijing representative office

Beijing, cn.boell.org en

中国改革论坛

[ China Reform Forum ]

Haikou City, crf.org.cn zh

Chinese Social Sciences Net

Beijing, cssn.cn en + zh

国务院发展研究中心

[ Development Research Center of the State Council ]

Beijing, drc.gov.cn zh

全国哲学社会科学工作办公室

[ National Office for Philosophy and Social Sciences Planning ]

Beijing, nopss.gov.cn zh

Our Hong Kong Foundation

Hong Kong, ourhkfoundation.org.hk en + zh

盘古智库

[ Pangoal Institution ]

Beijing, pangoal.cn zh

Tech :

China Academy of Information and Communications Technology

Beijing, caict.ac.cn en + zh

Urban Planning :

Urban & Innovation Environment Index

Guangzhou, uiei.org en

41 top French TECH think-tanks

Electronic Communications and Postal Regulatory Authority

arcep.fr en + fr

OPTIC

optictechnology.org en + fr

Renaissance Numérique

renaissancenumerique.org fr

Digital New Deal

thedigitalnewdeal.org en + fr

International Science Council

council.science en

Institut Sapiens

institutsapiens.fr fr

OECD.AI

oecd.ai en

AI-Regulation.com

ai-regulation.com en

Centre pour la Sécurité de l’IA

securite-ia.fr en

National Institute for Research in Digital Science and Technology

inria.fr/Artificial-Intelligence en

Institut Français des Relations Internationales

ifri.org/technologie/ en + fr

EU Cyber Direct

eucyberdirect.eu en

International Institute of Space Law

iisl.space en

Capgemini Research Institute

https://www.capgemini.com/high-tech en + fr

Hub France IA

hub-franceia.fr fr

Direction générale des Entreprises

entreprises.gouv.fr/numerique fr

Futuribles

futuribles.com/tech fr

Cigref

cigref.fr en + fr

Agence nationale de la sécurité des systèmes d’information

cyber.gouv.fr fr

Conseil national du numérique

conseil-ia-numerique.fr fr

European Science-Media Hub

sciencemediahub.eu en

INCYBER Forum

europe.forum-incyber.com fr

Association Nationale de la Recherche et de la Technologie

anrt.asso.fr fr

Human Technology Foundation

human-technology-foundation.org en + fr

Conseil national du numérique

conseil-ia-numerique.fr fr

Numeum

numeum.fr fr

La Mednum

lamednum.coop fr

Association Française pour le Nommage Internet en Coopération

afnic.fr fr

Labo Société Numérique

( Programme Société Numérique de

l’Agence Nationale de la Cohésion des Territoires )

labo.societenumerique.gouv.fr en + fr

Centre pour la Sécurité de l’IA

securite-ia.fr en + fr

EuroStack Directory Project

euro-stack.com en

European Parliament Technology Assessment

eptanetwork.org en

Avolta

avolta.io en

Société française d’énergie nucléaire

sfen.org fr

HOP – Halte à l’obsolescence programmée

halteobsolescence.org en + fr

Nuclear Transparency Watch

nuclear-transparency-watch.eu en

Agence nationale pour la gestion des déchets radioactifs

andra.fr fr

Autorité de sûreté nucléaire et de radioprotection

asnr.fr fr

World Nuclear Industry Status Report

worldnuclearreport.org en

Bureau de Recherches Géologiques et Minières

brgm.fr en + fr

Joint European Disruptive Initiative

jedi.foundation en